The National Development Plan (PND) 2021-2025 aims to make the manufacturing industry the backbone of the structural transformation of the economy.

The strategic objectives associated with this ambition include balanced development across regions through the implementation of industrial clusters, increasing the competitiveness of manufacturing industries, and enhancing foreign trade.

To achieve these objectives, the Government has implemented actions and reforms aimed at improving governance, productivity, and competitiveness in the manufacturing subsector through:

- the development and implementation of a strategic plan for the recovery of struggling companies (textile sector);

- the establishment of a dedicated area for the cement sector covering 59 hectares as part of the development of a 234-hectare plot (Phase 1) in the Akoupé-Zeudji PK24 industrial zone by Soroubat;

- the development of 127 hectares in MOP by the operator CHEC in the Akoupé-Zeudji PK24 industrial zone;

- the improvement of quality and the fight against counterfeiting; the reservation of 105,000 tons of cotton seeds for processors in favor of COTRAF (66,000 tons), AITTPA (24,000 tons), and APMUT (15,000 tons) in 2022 to meet their raw material supply needs;

- the completion of two studies in 2022 on industrial clusters (Textile and Clothing, Automotive Assembly) out of a total of seven (Agro-industry, Textile and Clothing, Construction Materials, Chemical Plastics, Pharmaceutical Industry, Automotive Assembly);

- the operationalization of the Industrial Infrastructure Management and Development Company named SOGEDI in 2023;

- the adoption by the Government of a strategic framework for the development of industrial zones in 2022;

- the raising of 5 billion FCFA in funds from banks for financing the material investments of 15 supported companies.

The industrial policy has identified seven (07) industrial clusters on which industrial development should be based, including agro-industry and six (06) others related to other manufacturing industries, namely the pharmaceutical industry; construction materials, furniture, and equipment; chemical and plastic industries; textiles; vehicle assembly and manufacturing of spare parts; and packaging.

To this end, industrial development relies on a dynamic legal and regulatory framework.

Notable mentions include:

- the adoption of law n°2013-866 of December 23, 2013, relating to standardization and quality promotion and its two implementing decrees;

- decree n°2015-22 of January 14, 2015, relating to the procedures and conditions for granting land for industrial use;

- decree n°2016-1152 of December 28, 2016, making certain standards mandatory;

- decree n°2017-145 of March 1, 2017, setting the conditions for establishing an industrial unit on land located outside an industrial zone;

- law n° 2018-985 of December 28, 2018, concerning the regime of free zones;

- ordinance n° 2020-687 of September 23, 2020, legalizing the tax and customs regime of the development agreement for the project of industrial economic zones in Abidjan, Ferkessédougou, and San Pedro;

- decree n°2022-245 of March 30, 2022, creating the "Industrial Infrastructure Management and Development Company," abbreviated as SOGEDI;

- decree n°2022-596 concerning the adjustment of the industrial fee in the industrial zones of Bonoua and Grand-Bassam dated August 3, 2022;

- decree n°2022-595 of August 3, 2022, concerning the adjustment of the payment modalities for the occupation fee of industrial land for industries processing logs in the industrial zones of Bonoua and Grand-Bassam. From an institutional perspective, several entities such as SOGEDI, OIPI, CI Engineering, CDT, I2T, and LANEMA are relied upon.

Main Strategic Indicators of the Industry Sector

|

Key Indicators |

Reference Situation |

Target |

||

|

Year |

Value |

2023 |

2025 |

|

|

Share of the industrial sector in GDP |

2019 |

21.2% |

24% |

28% |

|

Rate of rehabilitation of industrial zones to be rehabilitated |

2020 |

20% |

50% |

100% |

|

Global Competitiveness Index (GCI) World Economic Forum Global GCI Rank |

2019 2019 |

48.1 118th |

60 75th |

70 55th |

|

Number of developed industrial zones |

2020 |

04 |

08 |

10 |

|

Number of rehabilitated industrial zones |

2020 |

01 |

03 |

05 |

|

Satisfaction rate of industrial land requests |

2020 |

45% |

80% |

90% |

Source: PND 2021-2025

The industry constitutes the bulk of the formal private sector in Côte d'Ivoire.

This sector has experienced growth with an average annual growth rate of 8.3% over the period 2015-2019, 1.9% in 2020, and 11.2% in 2021. As for the value added by the sector, it increased from 5,291 billion FCFA in 2015 to 7,267 billion FCFA in 2019, and then to 7,365 billion FCFA in 2020.

Finally, the sector's share in GDP decreased from 25.2% in 2018 to 26% in 2019, 21.1% in 2020, and then to 21% in 2021. The total investments made in the industrial sector amount to 294.47 billion FCFA, distributed as follows: 69.59 billion FCFA in 2019 (23.6%), 68.48 billion FCFA in 2020 (23.3%), and 156.40 billion FCFA in 2021 (53.1%). These investments have led to the creation of a total of 58 companies and 3,116 direct jobs, distributed as follows: 21 companies for 1,520 jobs created in 2019, 9 companies for 394 jobs created in 2020, and 28 companies for 3,116 jobs generated in 2021.

The volume of industrial production in Côte d'Ivoire increased by 6.2% in 2021 compared to its level in 2020. This good performance in industrial activities is mainly due to manufacturing industries (+7.6%).

In 2022, the volume of production recorded an increase of 7.4% over the entire year, year-on-year, driven by the performance of extractive industries (+12.5%) and manufacturing industries (+5.4%).

In 2023 (the first five months), the volume of industrial production in the country recorded an increase of 7.1% compared to the same month in 2022. This growth in industrial production volume is mainly due to the good performance of manufacturing industries (+8.4%) and extractive industries (+3.7%), with respective contributions of 5.40 points and 1.05 points. This upward trend is primarily driven by manufacturing industries (+5.3%) and extractive industries (+5.4%).

Growth Rate of the Secondary Sector

|

Volume Change in % |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

Secondary |

5.3 |

15.4 |

4.3 |

11.5 |

1.9 |

7.4 |

10.4 |

|

Petroleum Products |

-180.9 |

0.0 |

-298.1 |

19.0 |

-25.7 |

23.9 |

-2.4 |

|

Mining Extraction |

16.9 |

-17.4 |

-38.2 |

17.5 |

6.2 |

0.5 |

3.8 |

|

Gold, including diamonds and other extractions |

6.6 |

3.8 |

7.7 |

-6.6 |

19.0 |

4.9 |

4.8 |

|

Manufacturing Industries |

-3.2 |

11.2 |

3.8 |

2.4 |

-0.8 |

6.3 |

6.1 |

|

Agro-food |

-20.8 |

9.6 |

-2.4 |

5.4 |

-7.0 |

2.6 |

3.3 |

|

Drinks and Tobacco |

62.3 |

11.6 |

15.4 |

15.4 |

9.5 |

16.9 |

10.7 |

|

Textiles and Clothing |

-9.7 |

-5.0 |

3.1 |

-0.5 |

-0.5 |

2.0 |

3.5 |

|

Wood, Paper, and Printing |

-18.9 |

-31.3 |

16.3 |

23.9 |

7.9 |

1.6 |

12.4 |

|

Chemicals, Rubber, Plastics |

297.7 |

91.1 |

1.3 |

0.1 |

16.7 |

8.6 |

7.1 |

|

Non-metallic Minerals |

47.1 |

-5.9 |

27.1 |

6.6 |

10.0 |

5.9 |

4.3 |

|

Furniture and Others |

3.5 |

9.2 |

6.8 |

-7.7 |

-5.9 |

9.2 |

7.1 |

|

Energy |

11.0 |

128.0 |

9.4 |

7.3 |

5.6 |

-4.7 |

17.2 |

|

Construction |

34.3 |

24.2 |

6.5 |

23.8 |

5.5 |

12.4 |

15.8 |

Source : MEF/MPD(INS)

Share of the Secondary Sector in GDP from 2015 to 2022

|

Share in GDP in % |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

Secondary |

19.5 |

19.1 |

20.5 |

21.0 |

21.2 |

20.9 |

21.1 |

21.2 |

|

Petroleum Products |

0.5 |

-1.6 |

-0.8 |

2.1 |

2.3 |

1.6 |

2.3 |

2.1 |

|

Mining Extraction |

3.3 |

5.0 |

4.2 |

2.8 |

3.0 |

3.3 |

3.1 |

2.9 |

|

Gold, including diamonds and other extractions |

1.9 |

2.3 |

2.0 |

1.4 |

0.9 |

1.4 |

1.0 |

1.3 |

|

Manufacturing Industries |

10.4 |

10.6 |

10.9 |

9.8 |

9.5 |

9.6 |

9.4 |

9.5 |

|

Agro-food |

5.4 |

5.2 |

5.2 |

4.1 |

4.1 |

3.7 |

3.5 |

3.3 |

|

Drinks and Tobacco |

0.4 |

0.3 |

0.3 |

0.3 |

0.4 |

0.4 |

0.6 |

0.8 |

|

Textiles and Clothing |

0.6 |

0.6 |

0.6 |

0.5 |

0.5 |

0.5 |

0.5 |

0.5 |

|

Wood, Paper, and Printing |

0.8 |

0.6 |

0.4 |

0.4 |

0.4 |

0.4 |

0.4 |

0.5 |

|

Chemicals, Rubber, Plastics |

0.2 |

0.4 |

1.2 |

1.2 |

1.1 |

1.3 |

1.3 |

1.4 |

|

Non-metallic Minerals |

0.3 |

1.0 |

0.9 |

1.0 |

1.0 |

1.0 |

0.9 |

1.0 |

|

Furniture and Others |

2.8 |

2.3 |

2.3 |

2.4 |

2.1 |

2.3 |

2.2 |

1.9 |

|

Energy |

0.9 |

1.1 |

2.5 |

2.6 |

2.7 |

2.5 |

2.2 |

2.1 |

|

Construction |

4.5 |

3.9 |

3.7 |

3.7 |

3.7 |

3.8 |

4.1 |

4.6 |

Source: MEF/INS

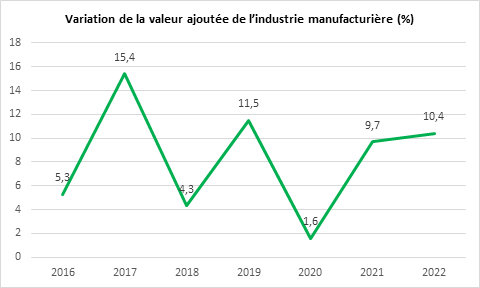

Regarding the manufacturing industry, it should be noted that the value added by the manufacturing industry in real terms has progressed erratically, respectively by 5.3%, 15.4%, 4.3%, and 11.5% between 2016 and 2019, and is estimated at 1.6% in 2020 and 9.7% in 2021 according to INS statistics.

In 2022, it is expected to grow by 10.4%. In terms of resource-employment of GDP, the manufacturing industry (including agro-food) represents 682.2 billion FCFA (2020), 713.4 billion FCFA (2021), and 774.8 billion FCFA (2022).

Furthermore, the pre-identification for the 2019 census conducted by INS reveals that the Ivorian industry has more than 8,500 companies; and the manufacturing industry (including agro-food) represents 72.4% of the secondary sector with agro-food and tobacco industry (32.1%); textile and leather industries (2.4%); wood and furniture industry (14.9%); paper, cardboard, and publishing, printing industry (3.3%); petroleum, chemical, and rubber, plastics industries (15.1%); metal industries (0.3%); and the manufacturing of machines and equipment of all types (4.3%).

Source: INS

The manufacturing industries (excluding agro-food) were dominated in 2017 by the chemical, plastics, and pharmaceutical sectors (43%), and materials (21%); while the assembly (12%), textile (12%), and wood and printing (11%) sectors were underrepresented. Manufacturing industries accounted for 25% of the country's exports in 2017, while imported manufactured goods represented 62% of imports, half of which was attributable to the assembly sub-sector.

In 2021, the performance of manufacturing industries was mainly due to petroleum refining and coking (+15.3%), chemical products manufacturing (+23.6%), beverages (+17.8%), furniture and mattresses (+18.1%), and textile manufacturing (+14.1%), mitigated by the decline in food product manufacturing (-6%) as well as "leather work and manufacturing of travel articles and shoes" (-7.5%).

In 2022, the manufacturing industries included, among others, activities in food product manufacturing (+7.8%), textiles (+41.5%), pharmaceuticals (+16.6%), and chemicals (+13.1%).

Finally, in 2023, due to a continuous increase in production volume in the branches "food product manufacturing" (+7.0%), "petroleum refining, coking" (+18.1%), "rubber and plastic work" (+8.1%), and "extraction of metallic ores" (+10.7%) with respective contributions of 1.44 points, 1.37 points, 0.95 points, and 2.06 points. In May 2023, the volume of production in manufacturing industries recorded an annual increase of 8.4%. This growth in the volume of manufacturing production is mainly supported by the divisions "food product manufacturing" (+14.7%), "rubber and plastic work" (+13.4%), "repair and installation of machines and professional equipment" (+67.7%), and "chemical product manufacturing" (+19.3%). However, during the same period, the divisions "textile manufacturing activities" (-39.7%) experienced a decline.

The assembly sector remains embryonic with sixty-two (62) companies mainly involved in the assembly of non-electric machines and equipment. Additionally, projects for the establishment of new vehicle assembly units are developing. In 2022, the IVECO Group, in partnership with the Abidjan Transport Company (SOTRA), inaugurated a vehicle assembly unit named "Daily Ivoire." In 2023, a second partnership agreement was signed with the Ashok Leyland group for the establishment of an assembly line for more than 1,700 vehicles of 5 different types.

The chemical sector is dominated by plastics and rubber, representing 72% of the sector's exports in 2017, followed by cosmetics (15%). The production of natural rubber is mainly held by the African Rubber Plantations Company (SAPH), the largest producer in West Africa; about fifteen processing units are deployed across the territory.

In terms of rubber, the production of natural rubber is 1,219,000 tons of dry rubber in 2022. The total capacity for first processing is estimated at 1,372,800 tons of dry rubber in 2022. The rate of first processing of dry rubber into granulated rubber is about 85% in 2022. The ongoing increase in capacities: 28 state-transformer agreements for natural rubber allow for a projected increase of 960,000 tons between 2019 and 2025. The rate of second processing is 2%. Finally, it should be added that the market for the chemical industry is dominated by the Hyjazi group and is competing with the offer from Sippec (Ivorian company of plastic and chemical products).

Evolution of the Rubber Transformation Rate

|

Designations |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

Production of Dry Rubber (Tons) |

453,040 |

606,420 |

624,139 |

780,051 |

955,571 |

1,100,386 |

1,320,076 |

|

Installed Capacities (Tons of Dry Latex / Year) |

595,120 |

678,700 |

704,000 |

739,200 |

1,160,740 |

1,372,800 |

ND |

|

Quantity Processed (Tons of Granulated Rubber) |

453,040 |

471,002 |

504,852 |

573,222 |

659,741 |

861,206 |

1,053,284 |

|

Transformation Rate |

100% |

77.67% |

80.89% |

73.49% |

69.04% |

78.26% |

79.79% |

Source: MCIPMME/DGin

The production of the pharmaceutical industry remains low and covers about 6% of national demand. The sector has nine (09) local manufacturers, with CIPHARM representing more than 60% of production; it also has three (03) wholesalers who import more than 90% of national demand. This subsector, dominated by CI-Pharm since 1986, is seeing the arrival of several groups such as Tridem Pharma in 2022 with a project to build a drug production plant at a total cost of 56 billion FCFA; the establishment of the Chinese group Fosun Pharma (with 02 production lines for pharmaceutical products in view); and SAIPH (Arab Pharmaceutical Industries Company), whose factory construction is expected to be completed by the end of December 2023.

In the construction materials sector, a strong growth in cement production has been recorded (15.4% average annual growth between 2013 and 2018) with the arrival of new key players such as "Dangote Cement CI," "Lafarge Holcim CI," and CIMAF. Production capacity has tripled, rising from 2.75 million tons in 2013 to 9 million tons in 2018. Additionally, the cement sector has experienced a remarkable evolution in recent years.

Indeed, the nominal production capacity of cement installed today is estimated at 17,000,000 tons compared to 2,400,000 tons in 2011 and 5,700,000 tons in 2017, representing an increase of 608% over the period 2011-2022. The number of active industrial units is 13. In terms of actual production, it reached 5,200,000 tons in 2020 compared to 4,300,000 tons in 2019 and 4,000,000 tons in 2018. This production rose to 6,000,000 tons in 2021. The number of direct jobs generated in the sector was 1,575 employees in 2019, 2,000 in 2020, and approximately 2,300 in 2022. Cement imports are limited, except by government exemption. Regarding the export of materials, they remain dominated (about 90% in 2017) by metallic products (iron, steel, and aluminum). SOTACI is the main player in the steel industry with a production capacity of 150,000 tons per year.

The textile, clothing, and leather sector is driven by the export of cotton fiber (80% in 2017), despite existing transformation potential.

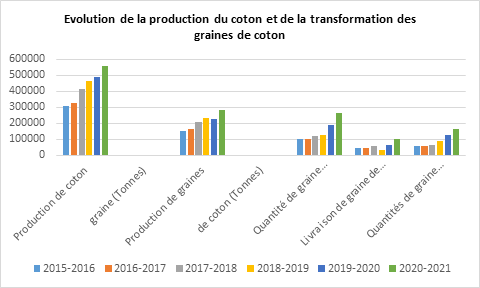

The production of cotton seed is 539,623 tons (Campaign 2021-2022). This makes the country the 2nd largest cotton producer in the sub-region. This production saw a drastic decline during the 2022-2023 campaign, reaching 239,183 tons against a forecast of 570,000 tons, due to attacks from harmful insects, the jassids.

However, rapid actions taken by the Council and Research have helped to curb this scourge, projecting a production of 400,000 tons of cotton seed during the 2023-2024 campaign. The sector counts three main spinning-weaving actors (FTG, COTIVO, and UTEXI), and two (02) actors in finishing (Uniwax and Texicodi), while the clothing sector is dominated by artisanal production with more than 50,000 actors against 15 industrial production units. Currently, the ginning capacity is 610,000 tons with 12 factories; and the processors consist of 5 ginning companies, 2 spinning units, and 3 large crushing units.

Source: MCIPMME/DGin

Variation in the value added of the manufacturing industry (%)

|

Year |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

Value |

5.3 |

15.4 |

4.3 |

11.5 |

1.6 |

9.7 |

10.4 |

Source : INS

Evolution of cotton production and cottonseed processing

|

CAMPAIGNS |

2015-2016 |

2016-2017 |

2017-2018 |

2018-2019 |

2019-2020 |

2020-2021 |

|

Cotton Production seed (Tonnes) |

310,081 |

328,155 |

412,646 |

461,197 |

490,423 |

559,483 |

|

Production of cotton seeds (Tonnes) |

153,614 |

164,000 |

206,323 |

231,663 |

229,131 |

280,903 |

|

Quantity of marketed seed (tonnes) |

103,331 |

100,000 |

123,000 |

126,048 |

190,136 |

262,443 |

|

Delivery of cotton seed to the local oil extraction industry (tonnes) |

46,585 |

44,100 |

60,500 |

34,708 |

61,511 |

99,936 |

|

Quantities of seed exported (tonnes) |

56,746 |

55,900 |

62,500 |

91,340 |

128,625 |

162,507 |

Source : MCIPPME/DGin