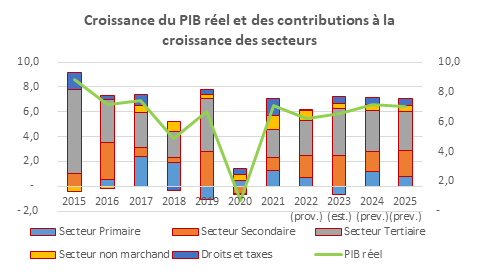

- Strong economic dynamism with an average growth of 8.1% over the period 2012-2019;

- Resilience to the shocks of the Covid-19 pandemic and the Russo-Ukrainian crisis;

- Estimated growth of 6.6% on average over the period 2021-2023;

- Growth primarily driven by the tertiary and secondary sectors, with respective contributions of 3.8% and 2.4% in 2023.

- Economy dominated by the services sector, which is estimated to account for 45.7% of GDP in 2023, down from 47.1% in 2016;

- Share of the secondary sector increasing from 20.8% in 2016 to 24.5% in 2023;

- Share of the primary sector declining to 14.4% in 2023 from 17.4% in 2016.

Sources : MEPD/DGE, ANStat

Structure of Supply

The Ivorian economy is characterized by a sectoral distribution in which services dominate, accounting for 45.7% in 2023 (excluding public administration production). The primary and secondary sectors represent 14.4% and 24.5% of GDP in 2023, respectively. Over the period 2024-2025, the supply is expected to be composed on average of 45.6% from services (excluding public administration production), 24.6% from the secondary sector, and 14.5% from the primary sector.

Evolution of Supply

In 2023, the growth rate was established at 6.5%, primarily driven by the secondary and tertiary sectors.

The Primary Sector experienced a decline of 4.1% in 2023 compared to an increase of 4.3% in 2022, related to the regression of export agriculture (-11.8%) despite the growth of subsistence agriculture (+8.5%), forestry (+0.4%), and fishing (+0.7%).

The Secondary Sector was dynamic with a growth of 10.3% in 2023 after an increase of 8.1% in 2022. This progression is linked to the rise of all its components, including construction and public works (+8.6%), energy (+19.8%), agro-food industries (+7.6%), other manufacturing industries (+7.6%), mining (+7.5%), and petroleum products (+20.0%).

The Tertiary Sector recorded a growth of 8.4% in 2023 compared to 6.3% in 2022, thanks to the increase in transportation (+9.3%), telecommunications (+8.7%), trade (+7.4%), and other services (+8.6%).

The Non-Market Sector increased by 4.7% after 8.8% in 2022, due to the combined effects of the strategy to control the wage bill and the continuation of policies for compulsory schooling and health for all.

Net taxes and duties after subsidies increased by 8.0% after 1.7% in 2022, thanks to the suspension of certain temporary measures taken in the context of combating inflation, as well as various administrative and fiscal policy reforms.

In 2024, the Primary Sector is expected to rebound (+8.3% compared to -4.1% in 2023), mainly linked to the increase in export agriculture (+10.4%), subsistence agriculture (+6.3%), and fishing (+0.2%).

The Secondary Sector is projected to grow by 6.6% in 2024 after the increase of 10.3% in 2023. This growth would be linked to the rise of all its components, including construction and public works (+10.1%), energy (+9.2%), agro-food industries (+6.8%), other manufacturing industries (+7.0%), mining (+5.1%), and petroleum products (+1.6%).

The Tertiary Sector is expected to grow by 7.3% in 2024 after the increase of 8.4% in 2023, thanks to the rise in transportation (+7.1%), telecommunications (+6.8%), trade (+6.7%), and other services (+8.0%). This dynamic would be driven by the performance of the primary and secondary sectors.

The Non-Market Sector is expected to grow by 5.4% after 4.7% in 2023, due to the combined effects of the strategy to control the wage bill and the continuation of policies for compulsory schooling and health for all.

Net taxes and duties after subsidies are expected to increase by 8.3% after 8.0% in 2023, thanks to various administrative and fiscal policy reforms as well as the dynamism of economic activity in a context of combating the high cost of living.

Real GDP Growth: Supply Perspective (in %)

|

Designation |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|||||||||||

|

def. |

def. |

def. |

def. |

def. |

def. |

prov. |

est. |

prev. |

prev. |

||||||||||||

|

Primary Sector |

3.1 |

13.7 |

11.4 |

-5.7 |

3.2 |

7.5 |

4.3 |

-4.1 |

8.3 |

5.4 |

|||||||||||

|

Secondary Sector |

14.6 |

3.7 |

2.0 |

21.4 |

-2.5 |

4.9 |

8.1 |

10.3 |

6.6 |

8.7 |

|||||||||||

|

Tertiary Sector |

7.3 |

5.9 |

4.2 |

6.6 |

-0.3 |

4.9 |

6.3 |

8.4 |

7.3 |

6.9 |

|||||||||||

|

Non-Market Sector |

-2.2 |

8.1 |

10.7 |

3.9 |

5.3 |

12.8 |

8.8 |

4.7 |

5.4 |

5.2 |

|||||||||||

|

Taxes and Duties |

5.0 |

12.2 |

-4.4 |

2.8 |

6.0 |

20.0 |

1.7 |

8.0 |

8.3 |

8.1 |

|||||||||||

|

TOTAL GDP |

7.2 |

7.4 |

4.8 |

6.7 |

0.7 |

7.1 |

6.2 |

6.5 |

7.2 |

7.0 |

Sources: MEPD/DGE, ANStat

Contributions of Sectors to Real GDP Growth (in %)

|

Designation |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|||||||||||

|

def. |

def. |

def. |

def. |

prov. |

def. |

prov. |

est. |

prev. |

prev. |

||||||||||||

|

Primary Sector |

0.6 |

2.4 |

1.9 |

-1.0 |

0.5 |

1.3 |

0.7 |

-0.7 |

1.2 |

0.8 |

|||||||||||

|

Secondary Sector |

2.9 |

0.8 |

0.4 |

4.1 |

-0.5 |

1.0 |

1.8 |

2.4 |

1.6 |

2.1 |

|||||||||||

|

Tertiary Sector |

3.5 |

2.8 |

2.0 |

3.1 |

-0.1 |

2.3 |

2.9 |

3.8 |

3.3 |

3.1 |

|||||||||||

|

Non-Market Sector |

-0.2 |

0.6 |

0.8 |

0.3 |

0.4 |

1.1 |

0.8 |

0.4 |

0.5 |

0.4 |

|||||||||||

|

Taxes and Duties |

0.4 |

0.9 |

-0.3 |

0.2 |

0.5 |

1.4 |

0.1 |

0.6 |

0.6 |

0.6 |

|||||||||||

|

TOTAL GDP |

7.2 |

7.4 |

4.8 |

6.7 |

0.7 |

7.1 |

6.2 |

6.5 |

7.2 |

7.0 |

Sources: MEPD/DGE, ANStat

Evolution of Nominal GDP - Supply Perspective (in billions of FCFA)

|

Designation |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|||||||||||

|

def. |

def. |

def. |

def. |

def. |

def. |

prov. |

est. |

prev. |

prev. |

||||||||||||

|

Primary Sector |

5,001.5 |

5,165.6 |

5,803.2 |

5,550.3 |

6,143.1 |

6,531.6 |

6,908.8 |

6,868.4 |

7,659.4 |

8,236.5 |

|||||||||||

|

Secondary Sector |

5,972.8 |

6,040.0 |

6,212.5 |

7,656.7 |

7,510.3 |

8,922.3 |

10,341.6 |

11,686.2 |

12,781.6 |

14,218.5 |

|||||||||||

|

Tertiary Sector |

13,523.4 |

14,708.1 |

15,584.5 |

16,590.2 |

17,041.4 |

18,389.3 |

19,692.4 |

21,840.0 |

23,901.0 |

26,187.6 |

|||||||||||

|

Non-Market GDP |

2,109.0 |

2,291.0 |

2,495.0 |

2,867.4 |

3,119.3 |

3,449.2 |

3,826.5 |

4,088.2 |

4,395.0 |

4,715.3 |

|||||||||||

|

Net Taxes and Duties |

2,080.0 |

2,287.0 |

2,411.0 |

2,714.0 |

2,463.8 |

3,074.5 |

3,001.9 |

3,308.1 |

3,654.4 |

4,029.4 |

|||||||||||

|

Nominal GDP |

28,686.7 |

30,491.6 |

32,506.1 |

35,379.0 |

36,278.0 |

40,366.9 |

43,771.2 |

47,790.9 |

52,391.3 |

57,387.2 |

Sources: MEPD/DGE, ANStat